If borrowers had their way, securing a loan with no money down would be simple. However, lenders prioritize risk management and typically mandate some form of down payment. But if you lack substantial funds upfront to secure a loan, there are still viable options available. Below, we’ll guide you through the essentials of obtaining various types of small business loans without requiring any upfront payment.

5 Best Small Business Loans With No Down Payment

Curious whether business loans necessitate a down payment? While some do, there are options that don’t. Securing a no-money-down business loan can be challenging and may lead to higher interest rates, but understanding each loan type can assist in choosing the best option for your needs.

1. Term Loans

Business term loans stand as one of the most prevalent financing solutions for small businesses, enabling access to substantial capital repayable over several years.

A notable advantage of term loans is that they often do not require an upfront payment. Instead, lenders may evaluate your creditworthiness and application, potentially requesting collateral or a personal guarantee.

In cases where the loan is used for acquiring commercial real estate or equipment, the lender may secure the asset itself as collateral. Interest rates for these loans are typically lower compared to alternative options and are typically offered to borrowers with stronger qualifications.

2. Equipment Financing

If you’re seeking funding to purchase or upgrade equipment for your business, you might not need an initial payment, as equipment financing can cover the entire cost, up to 100% in some cases. However, if the equipment depreciates quickly, lenders may not finance the full amount, requiring you to provide a down payment.

Additionally, because equipment financing uses the equipment itself as collateral, it’s often easier to qualify for compared to other types of financing. This makes equipment financing a viable option for new businesses or those with limited business credit history seeking their first business loan without requiring upfront capital.

3. Invoice Financing

Unlike loans that require fixed assets as collateral, invoice financing, a form of accounts receivable financing, does not necessitate a down payment. With invoice financing, you sell your outstanding invoices to the lender, using them as collateral.

This type of financing is particularly advantageous for businesses operating in the business-to-business sector with extended payment cycles.

4. Business Line of Credit

Business lines of credit offer a flexible financing option, especially useful if you lack collateral or funds for a down payment.

Here’s how they work:

- Business lines of credit are typically revolving, meaning once approved, you have a pool of funds available for borrowing.

- You can transfer money from the line of credit to your checking account as needed.

- Payments are required to cover the interest on the borrowed amount. Any additional payments reduce your loan balance.

- As you repay the borrowed amount, your available credit replenishes, allowing you to borrow again without reapplying each time.

5. SBA Microloans

Consider an SBA microloan if you’re seeking a startup business loan without upfront costs. These loans can go up to $50,000. While the SBA itself doesn’t mandate a down payment, SBA-approved lenders might.

Despite the potential for no down payment, SBA microloans typically necessitate collateral to secure the funding.

Providing a down payment on a small business loan inspires lender confidence.

Moreover, the more upfront money you can provide, the better. Higher initial payments decrease your repayment obligations and generally result in reduced rates and fees.

How Lenders Determine Down Payments

Securing a business loan without any upfront payment can be challenging as it provides less security to lenders. Even borrowers with excellent credentials may still be required to contribute cash to secure financing.

The amount of down payment required for a business loan depends on several factors:

Loan Type

Certain types of small business and commercial loans stipulate a specific percentage of the total loan amount to be provided as a down payment.

For instance, applicants for Small Business Administration (SBA) 504 loans are typically required to make a down payment ranging from 10% to 20%.

Principal Amount

The size of the loan principal significantly influences the down payment required for a commercial loan. Lenders perceive larger loan amounts as higher risks. While larger loans are typically offered to more qualified applicants, banks often require a down payment from borrowers to mitigate their own risk.

Term Length

Lenders understand that the longer borrowers take to repay a loan, the greater the risk of default. Therefore, securing long-term small business loans without a down payment is exceedingly challenging, if not entirely unfeasible.

Creditworthiness

Obtaining financing can be difficult without strong business and personal credit scores that demonstrate a reliable history of managing and repaying debts. Without this foundation, seeking a substantial business loan with no upfront investment may be impractical.

Lenders typically require a down payment if you lack a credit history or if certain factors have adversely affected your credit score. To improve your chances and secure more favorable loan terms, focus on building your business credit score over time.

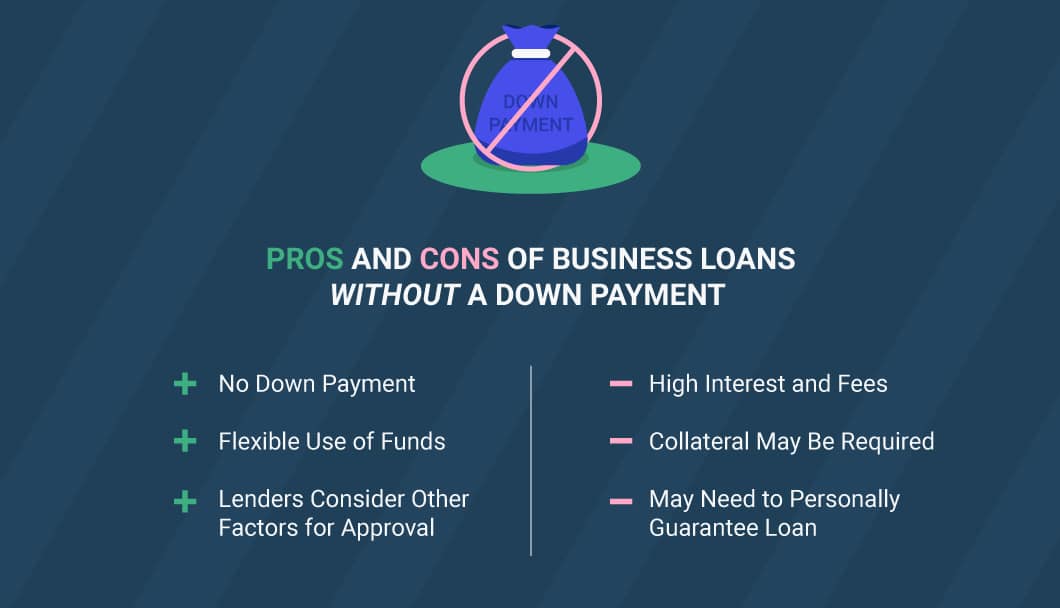

Characteristics of a No-Money-Down Business Loan

Loans that don’t necessitate down payments might seem ideal for borrowers, yet their terms often align with those offered to riskier applicants. Predictably, no-money-down business loans typically feature lower funding amounts compared to loans requiring a deposit. Moreover, terms tend to be shorter, and interest rates are generally higher.

To mitigate their risk, lenders may request collateral. This can involve using assets like real estate or equipment as security, ensuring repayment in the event of default.

Alternatively, lenders that don’t require specific collateral may opt for one or both of the following risk-mitigation strategies:

- Blanket lien: Enables a lender to claim all assets to settle the debt.

- Personal guarantee: Holds the guarantor personally liable if the business fails to repay its debt.

-

Alternative to a No-Money-Down Business Loan

While not classified as a traditional loan, a merchant cash advance provides financing without requiring upfront payments from borrowers. It stands out as one of the quickest methods for business owners to secure capital.

In this financing approach, approved applicants receive a lump sum of money based on their anticipated future sales. This short-term funding is typically repaid through daily installments.

Apply for a cash advance with no money down.

How to Get a Business Loan With No Money Down

When you’re exploring how to secure a commercial loan without upfront funds, start by clarifying your specific needs and objectives. Assess the various types of loans available to determine which best suits your situation.

For instance, if your goal is to acquire new equipment, explore equipment financing options. If you require funds to bridge cash flow gaps between client payments, consider invoice financing or a merchant cash advance. For launching a new business or supporting operational expenses, look into SBA microloans or business lines of credit.

When seeking a business loan without a down payment, evaluate the collateral you can offer. Remember, not having immediate cash available doesn’t eliminate your options. While it may pose challenges, obtaining a no-money-down business loan remains feasible.