Currently, small business loan rates can start as low as around 3% for highly qualified applicants at traditional banks, and go up to approximately 7% with online lenders.

The interest rate you receive for a business loan will depend on several factors, including the type of loan, the lender you choose, your credit score, and other relevant criteria. Finding the most competitive small business loan rates is essential for securing the financing needed for your company’s growth and strategic investments. By carefully evaluating these factors, you can identify the best loan options to support your business objectives.

Average Interest Rates for Business Loans

According to the latest Small Business Lending Survey conducted by the Federal Reserve Bank of Kansas City, the weighted average interest rates for small business financing range from 3.02% to 6.85%.

Among different types of small business loans, fixed-rate term loans, including Paycheck Protection Program (PPP) loans, have the lowest interest rates. On the other hand, variable-rate lines of credit tend to have the highest rates. Additionally, the interest rates for new term loans are generally higher than those for new lines of credit.

Interestingly, in the third quarter of 2021, most small business loan products experienced either an increase or stability in their weighted average interest rates, with the largest increase observed in fixed-rate term loans. This trend highlights the importance of closely monitoring loan types and their associated costs when seeking financing for small businesses.

Commercial Business Loan Rates Today at a Glance

Today’s average business loan interest rates can vary significantly based on the loan type, lender, and other factors. For example, variable business loan rates and lines of credit offered by traditional banks are generally tied to the prime rate (which was 7% as of November 2, 2022) plus an additional percentage. Secured business loans typically carry lower interest rates compared to unsecured loans due to the reduced risk for the lender.

Here are the interest rates and factor rates for popular business funding models offered by our partner lenders:

- SBA loans: Starting at 6% interest rate

- Medium-term loans: Starting at 7% interest rate

- Business line of credit: Starting at 8% interest rate

- Equipment financing: Starting at 8% interest rate

- Short-term loans: Starting at 10% interest rate

- Invoice financing: Starting at 1.02 factor rate

- Merchant cash advances: Starting at 1.10 factor rate

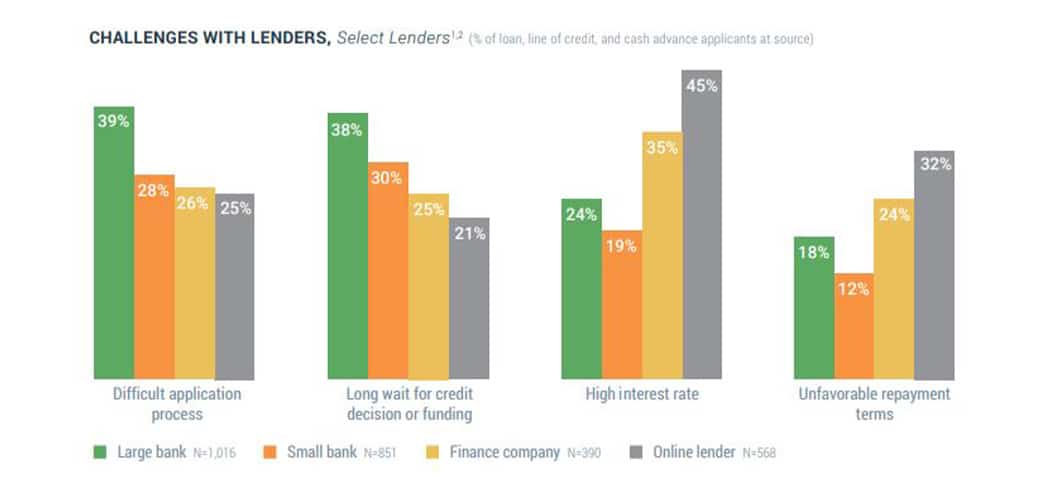

It is important to remember that conventional business loan rates are typically more competitive than those offered by online lenders. According to the Federal Reserve Banks’ 2022 Small Business Credit Survey, small banks are often preferred for their ability to provide lower interest rates, followed by large banks. However, these traditional lenders are known for their more rigorous application processes and longer wait times for credit decisions and funding.

By carefully comparing different loan types and lenders, you can find the best financing option that meets your business needs while minimizing costs.

Image Source: Federal Reserve Banks’ 2022 Small Business Credit Survey

Related: What Are the Current SBA Loan Rates?

Factors Affecting Business Loan Terms and Rates

Loan interest rates vary and are not universal. Generally, business loans with lower interest rates are typically offered to those with the strongest financial profiles.

When you apply for a small business loan, the lender evaluates several factors before determining the loan terms and interest rate. Here are some key considerations that can influence your loan interest rate:

- Credit Score: Both personal and business credit scores are crucial in the lender’s decision-making process.

- Industry: The nature of your industry can affect risk assessment and, consequently, the interest rate.

- Monthly Revenue: Consistent and strong monthly revenue indicates a reliable cash flow, positively influencing loan terms.

- Cash Flow: Healthy cash flow demonstrates your ability to manage loan payments.

- Time in Business: A longer business history can indicate stability and reliability.

- Collateral: Assets such as home equity or equipment can reduce the lender’s risk, potentially leading to lower interest rates.

Understanding these factors is essential, as they collectively shape the interest rate you may be offered. Lenders look at both your personal and business credit scores to gauge overall creditworthiness. The duration your business has been operational and your monthly revenue provide insights into your ability to manage loan repayments and your commitment to the business. Additionally, offering significant collateral can improve your chances of securing a loan with favorable terms.

Common Hidden Fees for Small Business Loans

Interest rates on small business loans are just one part of the overall cost. When you accept a financing offer, you may also encounter various additional fees. Some of the most common fees include:

- Application Fees

- Processing Fees

- Prepayment Fees

- Service Fees

- Late Payment Fees

- Closing Fees

- Guarantee Fees

- Origination Fees

Understanding these extra charges is crucial for effectively comparing business loan rates and making well-informed decisions for your business.

Certain fees, such as late payment or prepayment fees, act as penalties for deviating from the agreed repayment schedule. Others, like processing, application, and origination fees, compensate lenders for the administrative work involved in evaluating and approving your loan. Notably, an origination fee might reduce the amount of funds you actually receive from the loan.

Most lenders charge at least one of these fees, but the amounts can vary widely. For example, an application fee is often modest, typically a few hundred dollars or less. In contrast, an origination fee might be 1% to 2% of the loan amount and is usually deducted from the principal at closing.

It is essential to account for these additional fees alongside your business loan interest rate to get a full picture of your financial obligations. This comprehensive approach ensures you understand the true cost of borrowing and can compare different loan offers more accurately.

How to Find the Best Business Loan Interest Rates

When it comes to small business loan interest rates, conducting thorough research and exploring various lenders can be highly advantageous. Securing working capital is essential for many small businesses, and staying informed and proactive enables you to find the most competitive loan rates to support and grow your company.

By comparing offers from different lenders, you can identify the best rates and terms that suit your business needs. Understanding the various options available, including traditional banks, credit unions, and online lenders, can help you make an informed decision. Additionally, being aware of any additional fees and conditions associated with each loan can provide a clearer picture of the total cost of borrowing.

Being diligent in your search and comparing multiple loan offers not only helps you secure favorable interest rates but also ensures that you choose a financing option that aligns with your business goals and financial situation. This proactive approach is key to finding the best possible terms for your small business loan, ultimately contributing to your company’s success and growth.