The response depends on various factors because every business is unique. What suits your needs may not necessarily be suitable for another company nearby. Considerations include your business’s tenure, revenue, cash flow, and terms of loan repayment, among other factors.

Here are ten situations where it may (or may not) be appropriate to seek financing, along with key considerations when evaluating whether to take out a business loan.

When to Get a Small Business Loan

When considering the timing for a small business loan, we’re not referring to specific months like January or December. Instead, we’re discussing critical points in your business’s journey when seeking financing might be appropriate. Here are several scenarios where obtaining a loan for your company could be advantageous.

1. During Good Times

Certainly, loans are available to assist during financial hardships, but they’re not solely for those times. According to Forbes, the optimal time to secure a small business loan is preemptively, before urgent necessity arises. This proactive approach, termed proactive financing, occurs when your business is thriving, revenue is robust, and cash flow is healthy—factors that lenders prioritize.

2. If You Could Use a Buffer

Seasonal business owners often face challenges during slower months, making it difficult to sustain operations. During temporary cash-flow crunches, business financing can serve as a crucial source of working capital, bridging the gap until business picks up again.

3. While You Have Solid Credit

Certainly, while bad credit business loans are well-known, one of the most advantageous times to consider a loan is when your credit is in good standing. Typically, a higher credit score correlates with more favorable terms and lower interest rates when applying for a small business loan.

4. If You Need to Invest in the Business

When reinvesting in your business to foster growth, obtaining a business loan can be a strategic decision. This may involve expanding to a larger location, purchasing new equipment, acquiring bulk inventory, or hiring additional staff, among other opportunities.

5. When a Valuable Opportunity Knocks

Considering featuring a new product line or partnering with another brand? Grab your calculator and spreadsheets. Calculate the potential return on investment (ROI) for the opportunity beckoning you. Determine if a small business loan could facilitate transforming this opportunity into a profitable venture, boosting your revenue.

Related: Easily Calculate Business Loan ROI

-

Reasons Businesses Apply for Financing

According to the Federal Reserve Banks’ Small Business Credit Survey of 2022, reasons firms applied for financing included:

- Meet operating expenses, such as wages, rent and inventory (62%)

- Expand business, acquire business assets or pursue opportunities (41%)

- Refinance or pay down debt (30%)

- Replace capital assets or make repairs (29%)

When You Shouldn’t Get a Small Business Loan

Now that we’ve covered some instances when getting a small business loan could make sense, let’s look at when you should think twice.

1. When the Solution Doesn’t Match the Needs

Are you seeking short-term funding to address a long-term challenge? For instance, if you operate a cash-based business and are grappling with financial issues, you might consider financing as a solution. If your revenue is solid but you’re encountering recurring cash-flow problems, prioritize stabilizing your budget first. Alternatively, you could explore securing a loan to invest in professional bookkeeping services to manage your finances more effectively.

2. At a Time When You’re Overextended

If you’ve already taken out multiple loans or maxed out your existing line of credit, it might be time to reassess your financial strategy. While debt consolidation can be beneficial in certain situations, consistently relying on multiple loans and struggling with fund management suggests a need for a different approach. Rather than applying for additional loans and potentially exacerbating your financial situation, focus on improving your current debt management practices and overall financial management.

3. If You’re Uncertain About the Payoff of an Investment

When contemplating a small business loan, conducting thorough market research and performing an ROI analysis are essential steps. While you may envision the benefits, it’s equally crucial to identify and understand potential risks. It’s important to determine when your investment will start generating profits and the expected magnitude of those returns.

4. When You Want to Make a Costly Impulse Purchase

You think to yourself, I’ve got to have this, but ask yourself, do you really need that shiny object? Particularly if your business is just starting out, you might be better off initially steering clear of the glitz and glam and sticking to business essentials.

5. If You’re Looking to Fund Personal Expenses

It’s important to emphasize that business loans should never be used for personal expenses. Mixing personal and business finances, let alone personal and business debt, is highly discouraged. Many business lenders explicitly prohibit the use of funds for nonbusiness-related expenses in their contracts

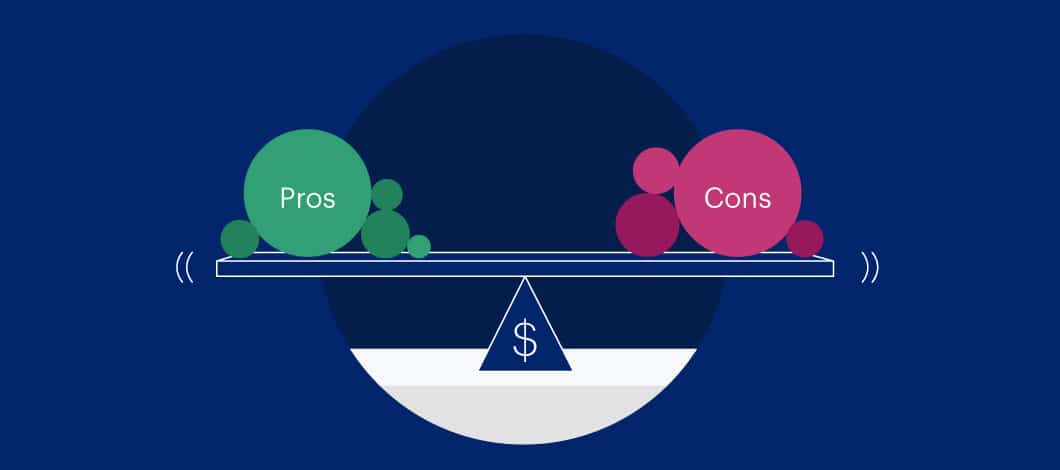

Business Loans Pros and Cons

The pros and cons of business loans can be broken down by many factors, including lender, loan type and repayment terms. That said, here’s an overview of general ones to keep in mind.

Pros

Retain Control of Your Business

Unlike investors who acquire a stake in your business, lenders do not. You retain full control over how you operate your company. Generally, unless specified otherwise in your lending agreement (such as with commercial real estate or equipment loans), you have flexibility to use your loan funds for various business-related expenses. Since you are not involving investors, you do not need to relinquish any equity, allowing you to maintain complete ownership and control of your company.

Build Your Credit

Occasionally, obtaining a small business loan can serve as a method for entrepreneurs to establish business credit. If your lender reports your payments to credit bureaus, you can enhance your credit profile by consistently making timely payments and managing your financing responsibly.

Get Through a Slow Season

Businesses often face ebbs and flows. During temporary downturns, entrepreneurs can utilize working capital loans to stabilize operations and navigate through cash-flow interruptions.

Cons

Shortages Can Arise

Conversely, if your payments are excessive and frequent, you could face cash-flow shortages, especially during revenue declines. When seeking business financing, it’s crucial to be honest with yourself about your financial situation.

Ask yourself what your business genuinely requires and realistically assess the payments it can afford. Additionally, ensure you fully understand the terms of any financing offers, including upfront fees, interest rates, payment schedules, and repayment terms.

Risk Equals Less Competitive Terms

When lenders assess loan applications, they carefully evaluate risk factors such as low credit scores, limited credit history, and existing debt levels to gauge creditworthiness.

Greater risk typically results in higher interest rates and shorter repayment periods. A higher interest rate means your loan will incur greater overall costs.

Debt Can Affect Business Valuation

Bank loans are counted as a business liability. Because they’re shown on a company’s balance sheet as a liability, a business’s valuation could be affected.

Risks in Taking Out a Business Loan

Personal Risk

If you struggle to make payments or default on your business loan, it can negatively impact your personal credit score. Additionally, if you provide a personal guarantee, you become personally liable for the business loan. This could potentially affect your ability to finance personal endeavors such as buying a vehicle, purchasing a home, refinancing a mortgage, and other financial plans.

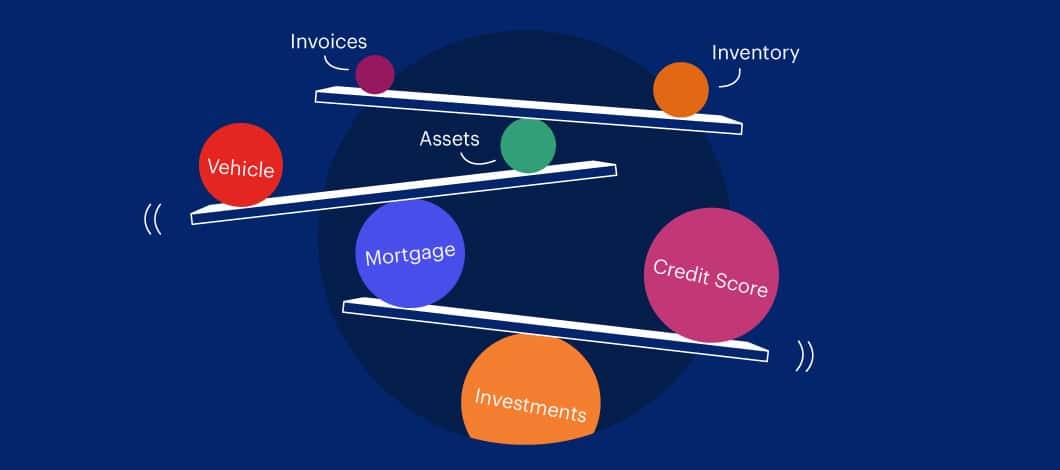

Collateral Obligation

Unlike unsecured loans, when applying for a secured business loan from a traditional lender like a bank, you typically need to offer collateral. Collateral can include assets such as real estate, inventory, vehicles, invoices, or investments. In the event of default, the lender can reclaim the pledged property to cover its losses.

Blanket Lien

In certain situations, lenders may file a blanket lien as a safeguard in case of default. This practice is typical with SBA loans and alternative financing options. Unlike specific collateral, a blanket lien enables financing entities to assert a claim over a broad range of a business’s assets, if necessary.

Related: Conventional vs. Alternative Lending

What to Consider Before Applying for a Business Loan

When deciding whether to take out a small business loan, carefully weigh the numerous factors involved and evaluate the advantages and disadvantages of business loans. Also, view your company from the perspective of a lender and assess the potential challenges in securing a loan. Factors such as your business’s tenure, revenue, cash flow, and credit score significantly influence the type of loan, amount, interest rate, and terms you may qualify for.