Lenders offer two primary types of loans to finance a company’s operations and expansion: simple interest loans and amortizing loans.

Both loan varieties require regular fixed payments on designated due dates, yet they differ significantly in their mechanisms for interest accrual and balance reduction.

Amortizing loans are characterized by fixed interest rates, typically quantified through an annualized percentage rate (APR). Conversely, simple interest loans often define interest costs using a factor rate. Each type is tailored to specific needs and purposes in funding operational requirements, each presenting unique advantages and drawbacks.

Let’s delve into how each method operates and determine which loan repayment schedule would best align with the financial needs of your business.

Understanding Amortized Loans

Amortized loans are commonly designed for long-term periods, often extending over three years or more, and involve regular monthly payments set at fixed amounts.

Each monthly payment is divided into two components: interest and principal repayment. Initially, a significant portion of the payment is allocated to cover interest charges, while the remainder goes towards reducing the principal balance. Over time, as the loan matures and the principal amount decreases, a smaller proportion of each payment is needed for interest, allowing more of the payment to directly reduce the principal owed. This gradual shift in payment allocation ensures that the loan is systematically paid off over its term.

Related: Amortization Schedule: What It Is – and How It Works

Example of a Amortized Loan

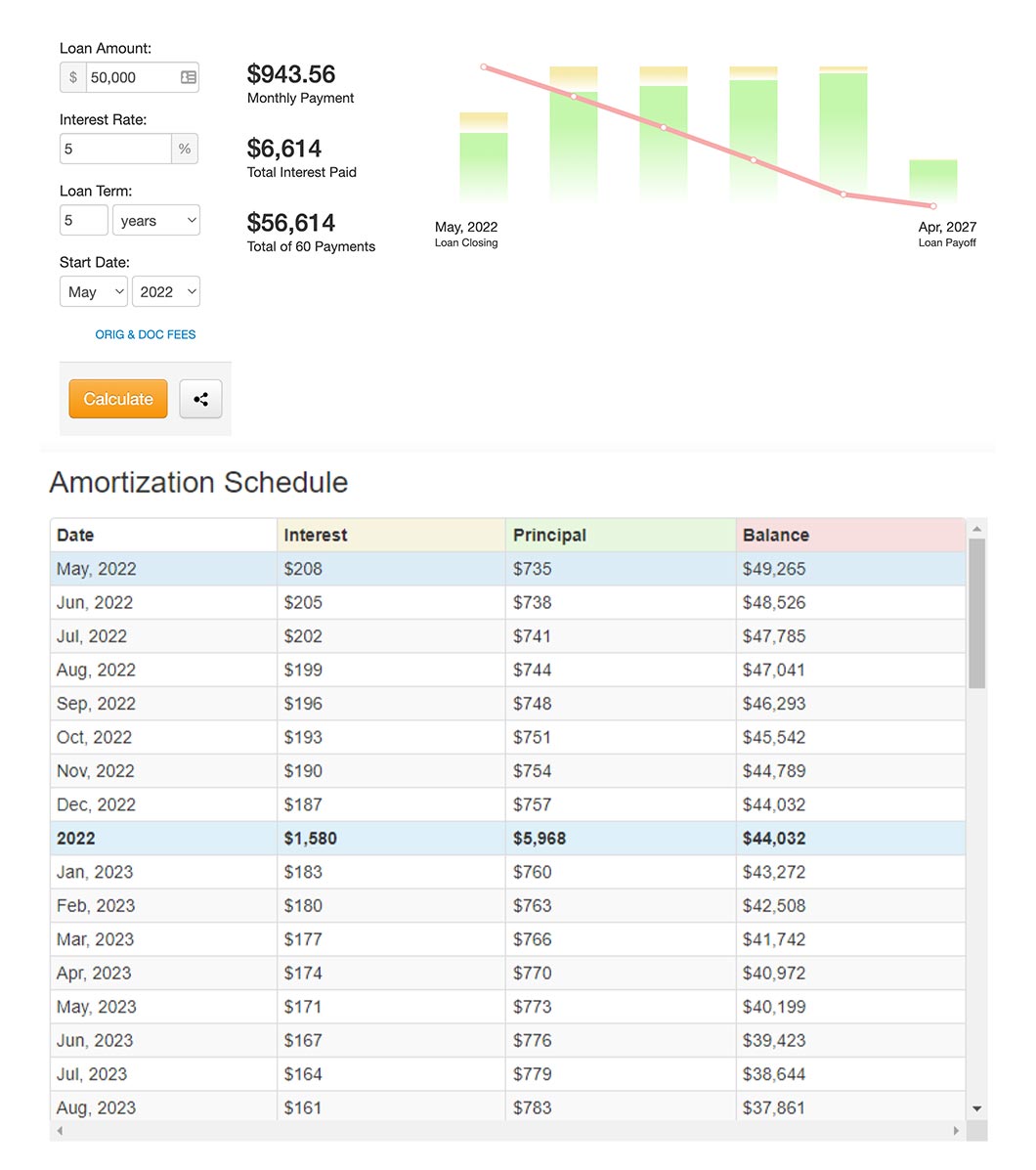

Let’s consider borrowing $50,000 at a fixed interest rate of 5% over a 5-year period. Using a loan amortization calculator, you’ll discover that your monthly payment remains consistent at approximately $944 throughout the 60-month term, covering both principal repayment and interest.

In the initial month, around $209 is designated for interest, with $735 applied towards reducing the principal balance, resulting in a new loan balance of $49,265.

Moving to the second month, the interest portion decreases to about $206 due to the reduced principal, while $738 continues to chip away at the principal amount. This lowers the balance further to $48,527.

This pattern continues as the loan progresses, with each payment reducing the principal balance and consequently lessening the interest portion. Over time, more of each monthly payment is directed towards paying down the principal amount. This process continues until the loan is completely repaid, bringing the balance down to zero.

Understanding Loans with Simple Interest

Simple interest loans are characterized by shorter durations, typically ranging from 6 months to 18 months, unlike the longer terms associated with amortized loans. Similar to amortized loans, they also feature fixed interest rates and regular fixed payments. However, the method of handling interest costs and principal repayments differs significantly.

In a simple interest loan, each payment throughout the loan’s duration comprises equal amounts allocated to both principal repayment and interest. This contrasts with amortized loans, where the interest recalculates based on the declining principal balance each period. Instead, the simple interest loan formula maintains consistent monthly payments that include both principal and interest portions without adjusting for the decreasing principal over time.

Example of a Simple Interest Loan

In contrast to amortized loans, which use interest rates expressed as percentages, simple interest loans typically specify interest as a factor rate, typically ranging from 1.0 to 1.9. Lenders determine this factor rate based on an evaluation of factors such as the company’s cash flow from bank statements, its longevity in business, and stable income as evidenced in tax returns.

For instance, if you borrow $50,000 with a factor rate of 1.2 for weekly payments over a 6-month term, you would repay the lender 1.2 times the principal amount, totaling $60,000. Of this total, $10,000 represents the interest cost ($60,000 total repayment minus the initial $50,000 advance).

Given that there are 26 weeks in 6 months, your fixed weekly payment, combining both principal and interest, would be approximately $2,307.70. This payment breaks down to $1,923.08 allocated towards repaying the original advance ($50,000 divided by 26 weeks) and $384.62 for interest charges ($10,000 divided by 26 weeks).

Unlike amortized loans where payments vary in their allocation between principal and interest over time, the payments for simple interest loans remain constant throughout the loan term.

Converting a Factor Rate to an Annualized Percentage Rate

When considering a factor rate, which is expressed as a decimal rather than a percentage, converting it to an annualized percentage rate (APR) can aid in comparing it with other loan options. However, when assessing short-term financing, APR might not always provide a straightforward comparison, especially for funding programs lasting less than a year.

To convert a factor rate to an annual percentage rate, let’s use our earlier example of a $50,000 loan:

- Calculate the percentage of financing costs relative to the original advance amount and multiply by 100 to convert it to a percentage:

$10,000 / $50,000 * 100 = 20%

- Multiply this percentage by the number of days in a year (365 days):

20% * 365 = 73

- Divide this result by the number of days in the loan term. For instance, if the loan term is 180 days:

73 / 180 = 0.4056

- Convert this decimal to a percentage to find the annualized percentage rate (APR). In our example, this translates to approximately 40.67%.

Therefore, in our $50,000 loan example with a factor rate of 1.2, the annualized percentage rate (APR) is approximately 40.67%. This calculation allows for a comparison of the potential annual borrowing costs of a simple interest loan with other alternatives, such as amortized loans.

Related: Short-Term Loans: Why APR Is the Wrong Metric

Differences Between Simple Interest and Amortized Interest Loans

In regards to simple interest vs. amortized loans, here’s a more detailed breakdown of what makes each unique.

Terms and Rates

Amortizing loans are generally structured with longer terms, often spanning several years, and commonly offer lower Annual Percentage Rates (APRs) compared to simple interest loans. In contrast, simple interest loans are typically shorter in duration, ranging from a few months up to about a year. Furthermore, as mentioned, simple interest loans often involve higher interest costs, which are typically expressed as a rate factor rather than a percentage.

The longer duration of amortizing loans allows for spreading out the repayment over a more extended period, which can result in lower monthly payments and overall borrowing costs. This makes them suitable for financing large investments or projects that require extended repayment schedules.

On the other hand, short-term simple interest loans are designed for quick financing needs where borrowers can repay the principal and interest within a shorter timeframe. While they offer flexibility and rapid access to funds, they generally come with higher interest rates due to the condensed repayment period and the use of factor rates rather than APRs for cost representation.

Understanding these distinctions helps businesses choose the most suitable loan type based on their financial needs, repayment capabilities, and the specific terms offered by lenders.

Collateral

Amortizing loans are commonly backed by collateral, such as equipment or vehicles, which provides lenders with additional security. This collateral serves as assurance that, in the event of default, the lender can recover some or all of the loan amount by seizing and selling the pledged assets. This feature lowers the risk for lenders, as they have recourse to recover their funds through the sale of the collateral.

In contrast, simple interest loans are typically unsecured and may rely more on the borrower’s creditworthiness and future sales projections for repayment. Because these loans lack collateral, lenders face higher risk, as there are fewer assets to seize and sell in case of default. This higher risk often translates into higher interest rates to compensate for the increased likelihood of non-repayment.

The distinction between secured amortizing loans and unsecured simple interest loans influences the terms and conditions offered by lenders. Businesses seeking lower interest rates and longer repayment periods may find secured amortizing loans more favorable, whereas those needing quicker, unsecured financing might opt for simple interest loans despite the higher associated costs. Understanding these differences helps businesses make informed decisions regarding their financing needs and risk tolerance levels.

Prepayment

Amortizing loans generally allow borrowers to prepay the principal amount without incurring penalties, offering flexibility to pay off the loan ahead of schedule and thereby reduce overall interest costs. This feature empowers borrowers to employ effective strategies, such as making additional small payments towards the principal alongside regular installments, which accelerates the loan repayment process.

In contrast, simple interest loans typically do not permit prepayment and may impose penalties for early repayment. For example, using our earlier scenario of a $50,000 simple interest loan, the borrower is obligated to repay a total of $60,000, regardless of whether the loan is settled in 1 month or 6 months. This lack of prepayment flexibility can limit borrowers’ ability to save on interest costs by paying off the loan early.

Understanding these differences in prepayment terms is crucial for businesses when choosing between amortizing loans and simple interest loans. It allows them to align their financing choices with their cash flow needs and strategic goals, whether it involves minimizing interest expenses or maintaining financial flexibility.

Time to Approval

Amortized loans often require a more extensive approval process. Lenders meticulously evaluate your financial statements and cash flow to gauge your company’s capability to fulfill loan obligations over the extended repayment period. This thorough assessment ensures that the loan terms align with the borrower’s financial health and ability to manage long-term debt.

On the other hand, simple interest loans are typically approved swiftly, often within hours or a few days. They undergo less stringent scrutiny compared to amortized loans since they are usually designed for shorter durations and involve higher interest rates to compensate for the reduced assessment of financial history and cash flow stability.

The differing approval processes reflect the varying risk profiles and repayment structures of amortized versus simple interest loans. Amortized loans prioritize thorough financial evaluation to mitigate long-term repayment risks, whereas simple interest loans emphasize quick access to funds with less detailed financial scrutiny. Understanding these distinctions helps businesses choose the appropriate loan type based on their financial situation, urgency of funding needs, and tolerance for approval timelines.

Choosing Between a Simple Interest and Amortization Loan

When deciding between a simple interest loan and an amortized loan, several factors come into play. One critical consideration is the intended use of the funds. For large purchases such as vehicles or equipment, an amortized loan is often preferred because its structured repayment schedule aligns with the asset’s useful life and depreciation over several years.

In contrast, if there’s an urgent need for funds to address short-term cash flow constraints, a simple interest loan may be more appropriate, despite potentially higher interest rates. These loans are typically approved swiftly, providing quick access to capital. For instance, a merchant cash advance exemplifies a type of simple interest financing that caters to immediate financial needs.

Personal and business credit ratings also significantly influence loan options. Businesses with lower credit scores may initially find it challenging to secure long-term amortized loans and may opt for short-term simple interest loans, even with higher interest costs, until their creditworthiness improves.

Regardless of credit rating, businesses must ensure they have adequate cash flow to comfortably manage debt payments, whether they choose amortized or simple interest loans. For those anticipating surplus cash flow and considering early loan repayment, it’s advisable to review any potential prepayment penalties associated with the loan terms.

By carefully weighing these factors—such as loan purpose, urgency of funding needs, credit profile, and repayment flexibility—businesses can make informed decisions that align with their financial goals and operational requirements.

Managing Your Company’s Debt Effectively

Effectively managing debt stands as a critical skill pivotal to enhancing your company’s growth and stability, or conversely, jeopardizing its financial standing. Collaborating with a lender who comprehends your business dynamics and can provide insightful guidance on appropriate financing options is essential.

There are occasions where a simple interest loan becomes necessary to navigate short-term cash-flow challenges swiftly. Conversely, when acquiring fixed assets like equipment or vehicles, an amortizing loan aligns with the asset’s lifespan, spreading repayment over an extended period.

Even if your initial credit score presents challenges, a supportive lender will work alongside you to finance your operations and contribute to building a positive borrowing history. They will analyze your cash-flow requirements thoroughly and suggest customized solutions tailored to your specific needs, fostering a constructive lending relationship.

By partnering with a lender who offers not just financial assistance but also strategic advice, businesses can navigate borrowing decisions effectively, ensuring they leverage debt to support growth while maintaining financial health and resilience.