You’ve decided to apply for a business loan, but where should you begin?

Knowing a lender’s business loan requirements before applying can streamline your application and speed up the underwriting process.

This guide will outline the typical commercial loan requirements and what steps you need to take to qualify for a business loan.

Business Loan Application Requirements

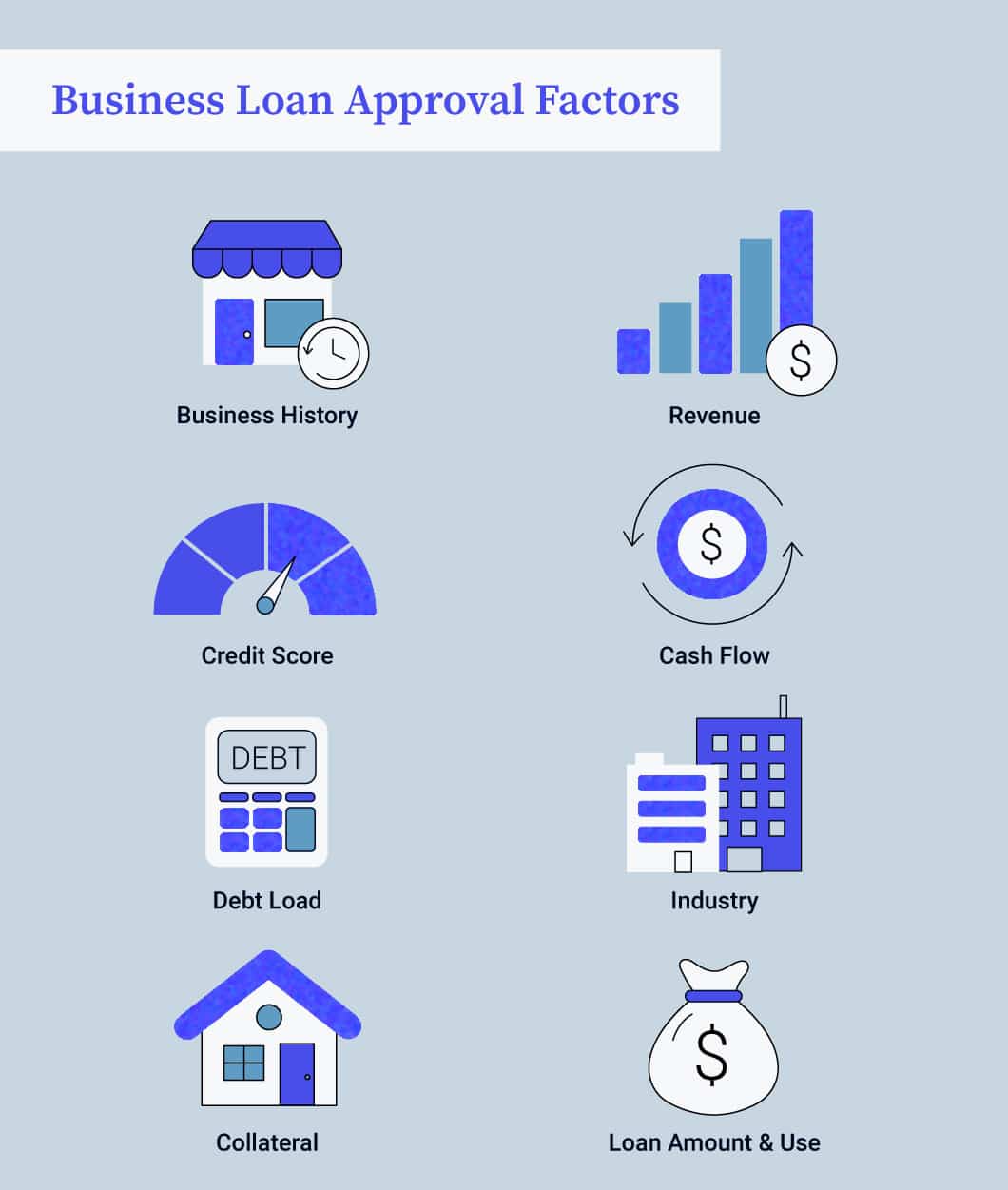

Several factors determine your eligibility for a small business loan. These requirements influence the amount of funding, the interest rate, and the repayment terms that the lender will offer.

While specific criteria vary by lender and type of financing, generally, lenders require the following information and documents to assess your application:

- Personal information

- Business information

- Time in business

- Annual revenue

- Cash flow

- Credit score and debt load

- Industry

- Collateral

- Business documentation

- Desired loan amount

- Intended loan use

1. Personal Information

One of the initial requirements for a small business loan application is your personal information. Lenders need details about you and any co-owners of your business. This information typically includes:

- Full name

- Social Security number

- Address

- Marital status

2. Business Information

Another one of the commercial loan requirements is basic information about your business. Lenders can ask for the following:

Full Business Name

Lenders require your business’s full name, including any DBA (“doing business as”) names if applicable, to search public records for information about your company. This includes checking for Uniform Commercial Code (UCC) liens filed with the Secretary of State office. An active lien indicates that other lenders have claims against your assets.

Employer Identification Number

If you are required to have one, an IRS-issued employer identification number (EIN) serves as your business’s Social Security number. Lenders use it to conduct a background check and verify the information you have provided about your company.

Ownership or Partnership Information

If you have business partners, you’ll need to provide their information as well. This helps the lender gain a comprehensive understanding of your company’s operations, each owner’s responsibilities, and how their credit scores and assets may affect the loan terms.

3. Time in Business

A major factor in business loan requirements is the length of time your business has been operating.

For instance, banks and Small Business Administration (SBA) loans typically require companies to have been in business for at least two years. Lenders prefer a proven track record of success, as established businesses are seen as less likely to default on a loan.

However, newer businesses still have options. Some financing solutions, such as merchant cash advances, are available to businesses that have been operating for less than a year.

4. Annual Revenue

Lenders want to see your annual revenue totals and examine details such as year-over-year differences and seasonal cash flow variations. Annual revenue requirements differ based on loan type and lender. For example, an SBA loan might require a minimum of $50,000 annually, while a business term loan could necessitate $200,000 or more in revenue.

Many lenders specify their revenue requirements on their loan product pages. For instance, Bank of America requires a minimum of $250,000 in annual revenue for a secured business line of credit, secured term loan, and commercial real estate loan. In contrast, its unsecured loans are available to businesses with at least $100,000 in yearly revenue. iBusinessLender indicates that its lending partners require $200,000 in annual revenue to qualify for a business line of credit.

5. Cash Flow

Besides revenue, lenders will examine your cash flow to assess your ability to repay the loan you’re seeking.

Even with high revenue, substantial expenses can result in insufficient cash flow to support a loan. The higher your revenue and cash flow, the better your chances of qualifying for a business loan.

Related: Cash Flow Loans for Small Business

6. Credit Score and Debt Load

Credit score, reflecting your credit history and debt load, is another key factor lenders consider when evaluating your loan application. Higher credit scores and a lower debt load improve your chances of approval. Although business and personal credit scores are distinct, lenders often consider both when assessing small business loan applications.

Personal Credit Score

While you’re seeking funding for your business, your personal credit score can significantly affect your ability to secure financing.

Banks typically require a personal credit score of at least 700, whereas SBA lenders may consider scores around 650, and alternative lenders might entertain applicants with scores in the 500s.

Your personal credit history serves as a gauge of your financial responsibility as an owner, reflecting your ability to manage money beyond your business. Even if your business’s financials are robust, a history of delinquencies or bankruptcies in your personal finances can raise concerns for lenders.

Business Credit Score

Your business credit score is another crucial factor lenders consider when evaluating your eligibility for financing. The specific small business loan credit score requirements can vary depending on the type of financing you seek. Generally, a score above 80 on a scale of 0-100 is considered very good.

A strong business credit score enhances your chances of approval for term loans with substantial amounts and favorable interest rates from banks and SBA lenders. Businesses with good credit often favor SBA loans due to their competitive terms and partial federal guarantee.

If your business credit score is less than ideal, there are still options available. Online lenders have made it easier to find small business loans for bad credit, expanding access to financing opportunities.

Small Business Tip

The best way to secure better rates and terms on your small business loan is by improving your creditworthiness. Being on time with payments and practicing better money management skills can repair your credit score and get you approved for affordable funding.

Related: What Credit Score Do I Need to Qualify for a Business Loan?

Debt Service Coverage Ratio

A significant aspect of evaluating your financial risk involves assessing your current debts.

Lenders calculate your debt service coverage ratio (DSCR) by comparing your existing debts to your business’s revenue. This ratio is critical in determining your ability to manage additional loan payments.

If your current debts and other financial obligations consume too much of your revenue, you may not qualify for another loan.

If you anticipate paying off a significant debt in the near future, it might be prudent to postpone applying for a small business loan.

Refinancing could potentially improve your DSCR. If your business has improved its credit profile since obtaining financing or if you secured initial funding as a startup, refinancing could offer better terms and lower payments.

7. Industry

Certain industries may encounter challenges when seeking business loans.

For example, businesses involved in activities such as gambling, loan packaging, speculation, investments, lending, leasing, insurance, pyramid sales plans, religious organizations, and rare coin and stamp dealing are typically ineligible for SBA loans.

Additionally, industries like commercial trucking and used car dealerships have higher failure rates, posing greater risks to lenders.

Furthermore, lenders assess sole proprietorships, partnerships, LLCs, and corporations differently. Your business structure dictates the additional information required for your loan application.

8. Collateral

When applying for a secured bank loan or an SBA-backed loan, providing collateral is typically necessary to secure the financing.

Collateral can take various forms such as cash, inventory, real estate, equipment, or accounts receivable. Securing a loan with collateral reduces the risk for lenders, often resulting in lower interest rates.

For unsecured business loans that do not require collateral, lenders usually require a personal guarantee. In some instances, even collateral-backed loans may necessitate a personal guarantee. This means you are personally responsible for repaying the lender if your company defaults on the loan.

9. Business Documentation

Commercial loan requirements involve providing specific documents that illustrate your business’s present condition and future prospects. Lenders typically ask for several months to up to two years of financial records, as well as the following information:

- Business plan

- Balance sheets

- Commercial property lease or deed

- Business licenses and permits

- Personal and business tax returns

- Profit-and-loss statements

- Accounts receivable and accounts payable statements

- Corporate documents (e.g., articles of incorporation, bylaws)

10. Loan Amount

One of the initial inquiries from a lender is, “How much funding do you require?”

The requested loan amount plays a crucial role in determining the type of financing and lender suitable for your needs. Larger banks typically concentrate on business loans exceeding $50,000, while online lenders are flexible, though they may have upper limits ranging from five to six figures.

It’s important to note that certain business loans may necessitate a down payment, sometimes as much as 20%. However, options like business lines of credit and accounts receivable financing often do not require a down payment.

11. Loan Use

It’s crucial to clearly outline how you intend to utilize the funding to advance your business.

If you’re acquiring a tangible asset like commercial real estate, you’ll need to furnish essential details about it. This might include the address, square footage, and photographs for an office space. Alternatively, if you’re purchasing equipment such as a commercial truck, you’ll typically need to provide details like mileage, maintenance history, and information about the dealership.

When applying for a working capital loan to enhance various aspects of your business, you must specify the precise purposes for which the funds will be used.

Lenders rely on this information to assess the potential returns on investment and how this will impact your ability to repay the loan.

Small Business Loan Requirements by Financing Type

When exploring the loan application process and the requirements for a small business loan, it’s crucial to note that these requirements vary depending on the lender and the type of financing.

Here’s an overview of what you can anticipate from various lenders, including iBusinessLender’s funding partners.

SBA Loan Requirements

SBA-backed loans are designed for small business owners who don’t meet bank loan requirements but still have strong creditworthiness.

To qualify for an SBA loan through iBusinessLender, you’ll need:

Do you qualify?

-

Credit score above

650+

Credit score above

650+

-

Time in Business

2 years +

Time in Business

2 years +

-

Annual Revenue

$50,000+

Annual Revenue

$50,000+

Business Lines of Credit Requirements

A business line of credit provides flexible, revolving funding that you can access as needed and repay in installments, much like a business credit card. Compared to term loans, business lines of credit typically have lower requirements, making them ideal for newer businesses with continuous working capital needs.

To qualify through iBusinessLender, you’ll need the following:

Do you qualify?

-

Time in Business

1+ year

-

Annual Revenue

$200,000+

-

Credit Score

560+

Equipment Financing Requirements

Equipment loans are secured by the equipment you’re financing, which can make them easier to qualify for.

With iBusinessLender, you’ll need to meet the following business loan requirements:

Do you qualify?

-

Time in Business

2+ years

-

Annual Revenue

$160,000+

-

Credit Score

620+

Accounts Receivable Financing Qualifications

Accounts receivable financing, also known as invoice financing, involves receiving an advance on your future receivables. Lenders use your accounts receivable aging statements to gauge how quickly they can expect repayment from your customers.

Because the advance is secured by your invoices, minimum requirements are relatively modest.

To qualify through iBusinessLender, you’ll need the following:

Do you qualify?

-

Time in Business

1+ years

-

Annual Revenue

$150,000+

-

Credit Score

600+

Merchant Cash Advance Requirements

A merchant cash advance (MCA) is secured by your future revenues. Repayment typically occurs daily or weekly, with payments deducted as a percentage of your credit card sales or through ACH debits from your bank account.

MCAs generally have the lowest minimum qualifications among alternative lending products.

To qualify for an MCA through iBusinessLender, you’ll need to meet these minimum requirements:

Do you qualify?

-

Time in Business

4+ months

-

Annual Revenue

$100,000+

-

Credit Score

500+

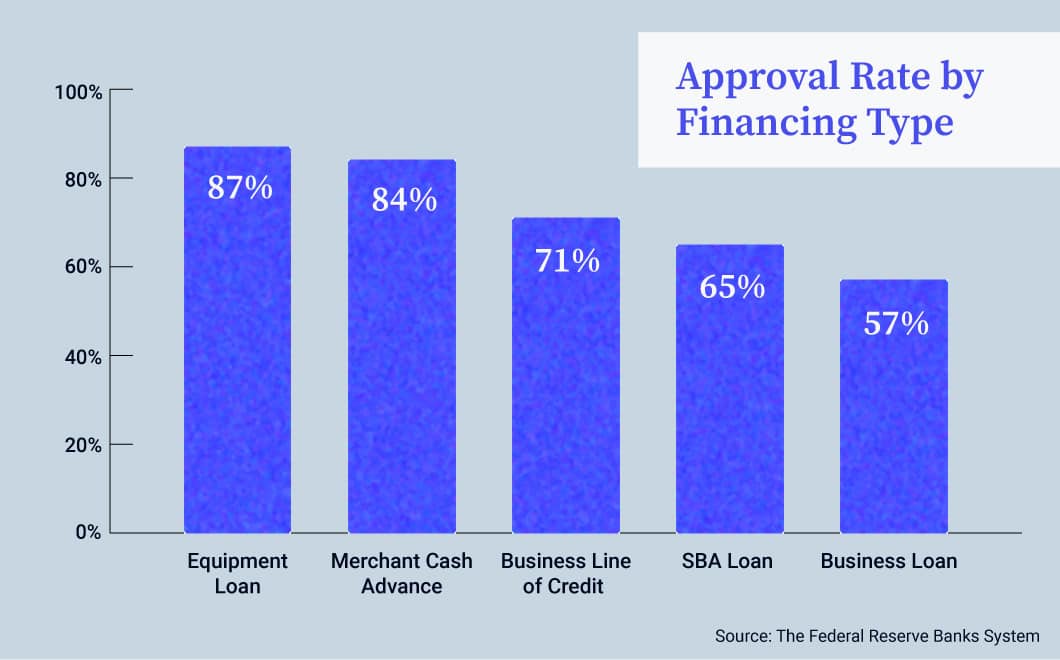

According to the Federal Reserve Banks System, business owners were most likely to be approved for an equipment loan (87%) followed by a merchant cash advance (84%) in 2020.

Requirements for a Startup Business Loan

If you’re launching a new business but face a funding shortfall, your options are more limited compared to established businesses. However, there are avenues available, such as the SBA microloan program. This program offers loans up to $50,000 with a maximum term of 8 years. Microloans are facilitated by community-based lenders and are accessible to applicants with new businesses, poor credit, or lower revenues.

Loan requirements vary by lender, but typically, you’ll need to provide the following documents and information:

- Personal information

- Credit score

- Bank account details

- Business plan

- Business licenses and certifications

If you find it challenging to meet startup business loan requirements, alternative options include opening a business credit card, applying for a personal loan, or seeking investors to kickstart your business venture.

What Do You Need to Get a Business Loan?

Traditional and alternative (online) lenders have distinct requirements when it comes to small business loan applications.

Traditional lenders, such as banks and credit unions, typically have more stringent approval criteria. Their loan requirements generally include the following:

Do you qualify?

-

Time in Business

2 years +

-

Revenues

Consistently high

-

Credit Score

700+

Traditional lenders also demand more extensive documentation and details about your business, often requiring in-person meetings and on-site visits before approving your loan application. This thorough vetting process and paperwork volume can lead to a longer timeline from application submission to approval and funding, often spanning several weeks to over a month.

In contrast, online lenders offer funding products that typically require less documentation. Business owners can complete their loan applications online and submit them within minutes. The small business loan requirements from online lenders generally include:

- Personal information

- Business information

- Bank account details (some lenders offer direct funding or withdrawals by connecting to your business bank account)

Credit score and revenue thresholds vary depending on the type of financing, but alternative lenders generally have more lenient criteria compared to traditional banks or credit unions. For instance, some borrowers may qualify for a merchant cash advance with a credit score of 500 or higher and annual revenue as low as $100,000.

The streamlined online application process accelerates the review and approval stages. Applicants can often receive approval within days, sometimes within hours, and funding on the same day.